The Covid-19 epidemic has exposed poor leadership and governance worldwide. From Spain to the U.K. to the U.S., politicians have waited far too long before taking the dramatic steps needed to protect their citizens.

Greece has been one noticeable — and perhaps surprising — exception to this trend. The government imposed severe social distancing measures at a much earlier stage of the epidemic than other southern European countries. For now, this swift reaction has helped Greece avoid the tragic healthcare crisis that richer states are facing.

Takis Pappas, a political scientist at the University of Helsinki, has compared the speed of the response in Greece, Italy and Spain. Athens closed down all non-essential shops only four days after reporting its first Covid-19 death. In contrast, Italy and Spain did so after 18 and 30 days, respectively. A ban on non-essential movement in Greece came only a week afterwards — faster than in either of the other two countries.

Those early actions reduced the pressure on the country's precarious healthcare system. In mid-March, the Greek national health system (ESY) could only count on 605 intensive care units, of which only 557 were in operation due to staff shortages. Greece has a population of more than 10 million people. That's a worse ratio than that of Spain, which started with 4,400 ICUs for a population of nearly 47 million and has been overwhelmed by coronavirus cases.

The comparison with Spain is telling. Even though Italy should have adopted lockdown measures sooner, politicians can argue that they were the first in Europe to deal with this unprecedented challenge. The Spanish government, on the other hand, had the benefit of time but dithered, letting mass events, such as demonstrations and football games, occur up to 26 days after the first Covid-19 death.

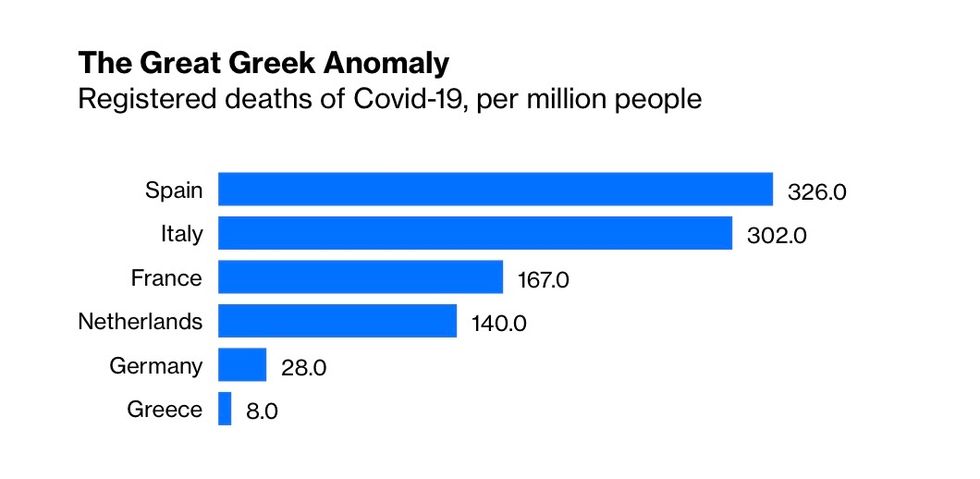

The Great Greek Anomaly

Registered deaths of Covid-19, per million people

Source: https://www.worldometers.info/coronavirus/

So far, Greece has registered only 1,955 cases and 86 deaths — that is 188 cases and 8 deaths per million people. Spain has 3,261 cases and 326 deaths per million people, and Italy has respectively 2,375 and 302. This may be because Greece has performed less than half as many tests (per million people) as Spain has, and less than a quarter as many as Italy, but there are no signs that the pressure on its health-care system is comparable to that experienced by the latter two countries. The Greek government also says it has recruited 4,200 new doctors and increased by half the number of ICUs, which should help contain a worsening of the outbreak.

Prime minister Kyriakos Mitsotakis has emerged as a voice of reason on the international stage. For example, he slammed Brazil's president Jair Bolsonaro for denying the gravity of the pandemic. Greece's political system as a whole, including the main opposition party Syriza, has reacted with composure — a very different picture to the bitter infighting that has emerged in Spain. And the Greek population appears to be very mindful of respecting the lockdown rules, in part a result of the government's steep penalties for non-compliance.

More worrying is what could happen to Greece's economy. The pandemic has come at a particularly cruel time for Athens. After a decade of economic crisis, things were finally getting back on track. Prime Minister Mitsotakis, of the center-right New Democracy, won an absolute majority in the 2019 elections, on a mandate to restore international credibility and shake up the economy. Investors flocked to Greece in search of returns and opportunities, making the Athens stock exchange the best-performing in the world last year.

That world could not look further away now. Tourism represents one-fifth of the country's total output and the industry will suffer badly if travel restrictions continue into the summer. Small businesses, which employ more than 80% of the country's total workforce (excluding finance), also face problems with supplies, liquidity and sales.

However, given how quickly Greece responded to the outbreak, the country might be able to get back on its feet sooner than others. Unlike in previous rounds of quantitative easing, the European Central Bank has decided to include Greek bonds in its 750 billion-euro ($810 billion) asset-purchase scheme, which is aimed at supporting the euro zone economy throughout the pandemic. It has also relaxed its rules, so that banks will be able to post Greek sovereign debt as collateral when they take up liquidity from the central banks. These were wise decisions and will provide additional stability for the country's financial markets.

For years, much of Europe has looked down on Greece as an insolvable problem. For all its intrinsic frailties, in this pandemic, Athens can walk with its head held high.

Ferdinando Giugliano writes columns and editorials on European economics for Bloomberg View. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

April 10, 2020

###

April 11, 2020

Voices4America Post Script. Share this information. #TrumpLiedPeopleDied Where leaders acted...Greece, New Zealand, Germany, others, #RealLeadersSaveLives

And then, there is this.